A founder's most dangerous document: explained

Five term sheet clauses. Most founders sign them without reading. Here is what they actually mean.

Read time: 6 min

A founder I know signed a term sheet in 2023. Smart person. Well-advised. Moved fast because the market was hot.

Two years later, when the company sold, she walked away with almost nothing.

The liquidation preference she did not fully understand had done its work. The investor got 2x their money back before she touched a cent.

This is not a rare story. It is the default outcome when founders sign documents they have not modelled.

The clauses nobody explains properly

Most first-time founders read a term sheet the way most people read a privacy policy. They skim it. They trust the investor is reasonable. They sign.

That is not naivety. It is information scarcity. Term sheets are written in a dialect of English designed, consciously or not, to obscure what is actually being agreed to.

Here are the five clauses that consistently cause the most damage.

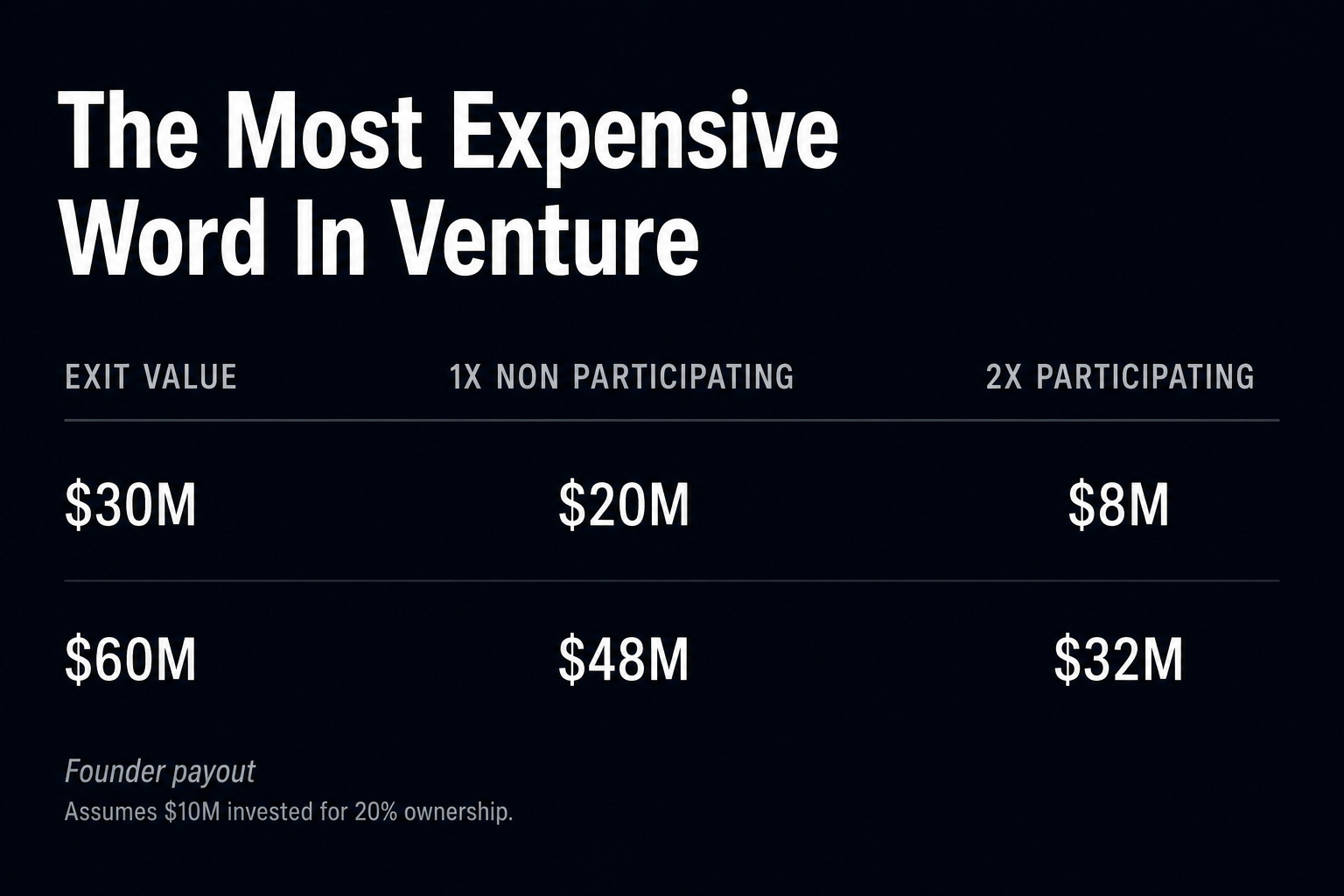

Liquidation preference

This determines who gets paid first, and how much, when the company exits or winds down.

A 1x non-participating preference means the investor gets their money back before founders and employees see anything. That is standard and fair.

A 2x participating preference means the investor gets twice their money back, and then continues to share in the remaining proceeds alongside everyone else. That is a different deal entirely.

The word “participating” is the most expensive word in early-stage venture. If your term sheet says “participating,” model the exit economics at every valuation you think is realistic. The math will surprise you.

Pro rata rights

The right for an investor to maintain their ownership percentage in future rounds by investing again.

This sounds harmless. It is not harmless when it is a “super pro rata” right, which allows an investor to take a larger stake than they currently hold. It concentrates ownership and can create serious tensions with new investors who want a clean cap table.

Read the definition precisely. “Pro rata based on fully diluted ownership” and “pro rata based on issued shares” are not the same number.

Drag-along rights

If a majority of shareholders votes to sell the company, drag-along rights force the minority to vote the same way.

In theory, this prevents a small group from blocking a deal the majority wants. In practice, look at who controls the majority. If it is the investor, they can effectively force a sale you do not want, at a price you do not want, at a time you do not want.

The key question: whose consent is required to trigger the drag?

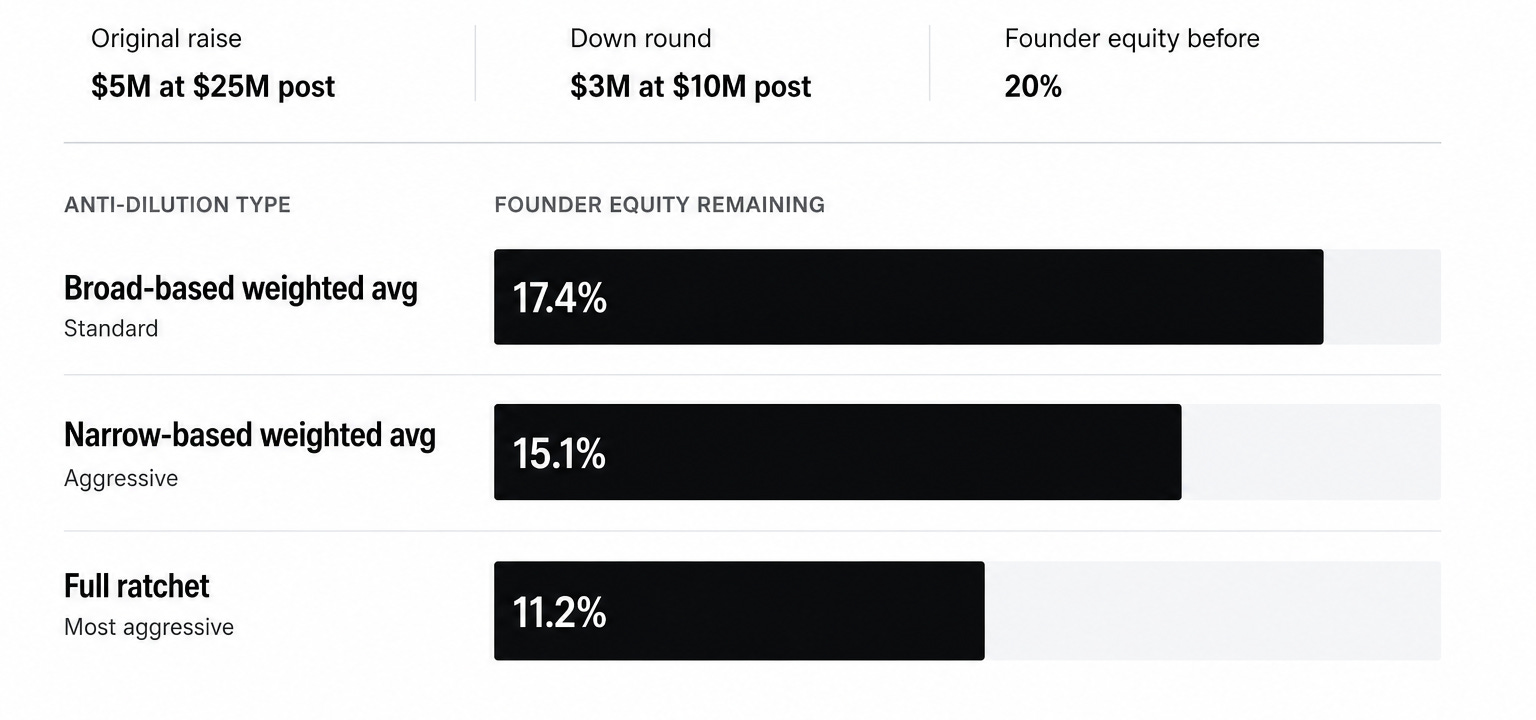

Anti-dilution provisions

If you raise a down round, anti-dilution provisions adjust the investor’s conversion price downward. They get more shares. You get diluted.

Full ratchet is the most aggressive version. Broad-based weighted average is standard. Narrow-based weighted average sits in between.

Most founders do not realize that “standard anti-dilution” can mean very different things depending on which standard is being applied.

Pay-to-play

A clause requiring existing investors to participate in future rounds or face conversion of their preferred stock to common.

This can actually protect founders. It prevents investors from sitting on preferred rights without continuing to support the company. But pay-to-play provisions vary enormously in how they are structured. Who decides what a “qualified financing” is? What triggers conversion? What are the threshold amounts?

The detail is in the definitions.

The real problem

These five clauses are not exceptional. They are in almost every institutional term sheet.

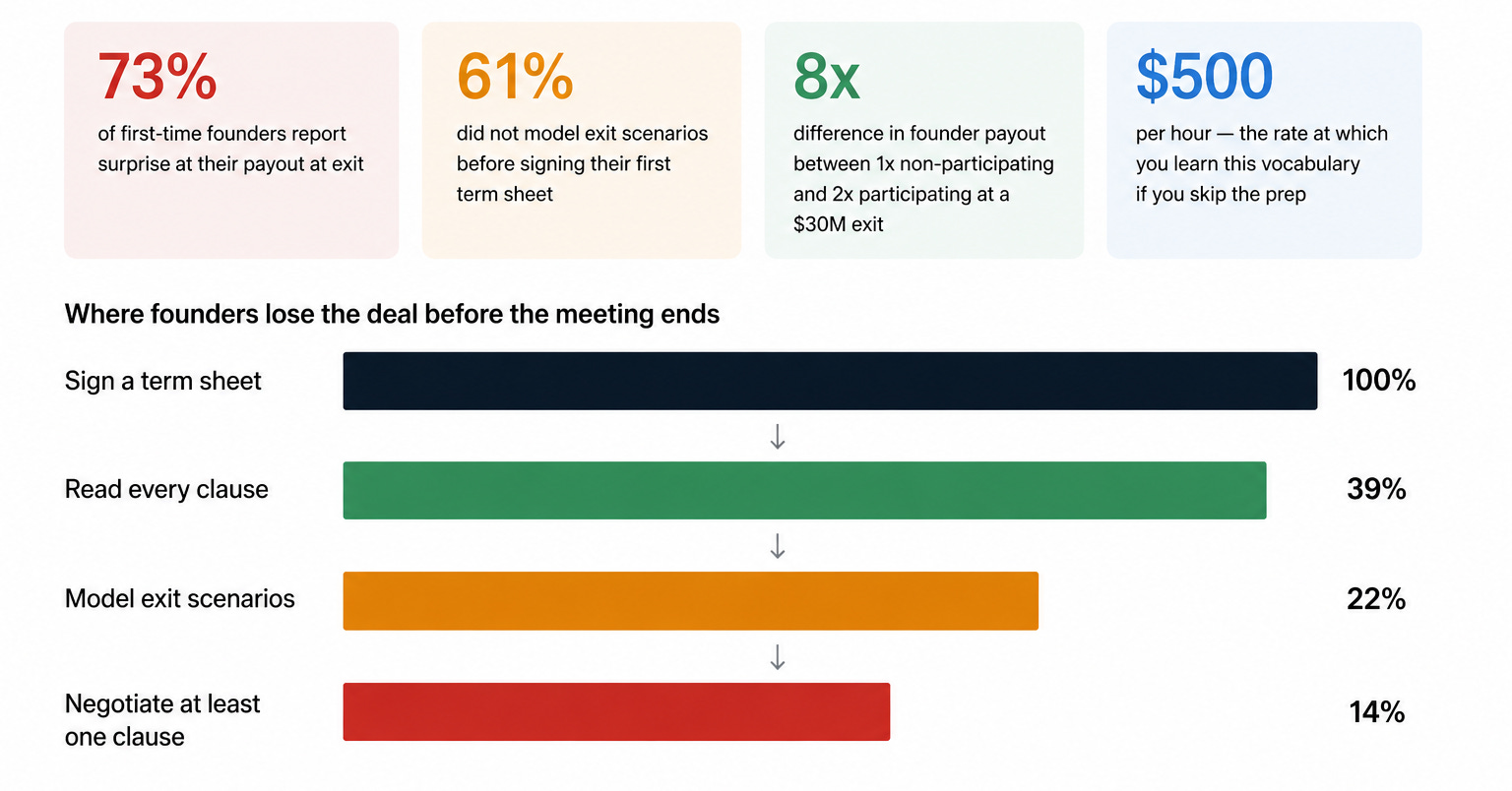

The problem is not that they exist. The problem is that most founders sign them without modelling what they actually mean at different exit outcomes. A $30M exit hits differently depending on your preference stack. A $3M bridge at a 20% discount does not feel urgent until you are raising your Series A and realize what it did to your cap table.

The resource below does what a good lawyer would do if you had unlimited time and a very patient attorney: it explains every clause, flags the red versions, and shows you exactly what to negotiate and how hard to push.

The full term sheet decoder

This is the premium resource. Everything above is the introduction.

Below is what I wish had existed before I sat across from my first institutional investor.

The document covers all 40 standard clauses explained in plain English with no assumed legal knowledge. Negotiation notes for each clause covering what is movable, what is not, and when to push back. Red flag annotations by investor tier across seed angel, institutional seed, and Series A funds. A side-by-side comparison of YC SAFE terms vs. priced round terms across 12 key dimensions. The 8 clauses that most often cause founder regret at exit, flagged throughout. And a negotiation guide covering the eight non-negotiables, the context-dependent clauses, and the one question to ask every investor before you sign.

This is not a legal document. It does not replace a lawyer.

It is the preparation you do before you pay the lawyer, so you are not learning the vocabulary at $500 an hour.

If you found this useful, these three are worth your time:

300 names on your list. Maybe 30 that matter. The three filters that take your investor list from 300 to 30. How to find the climate partners who are actually writing cheques right now.

VCs know in 90 seconds. Here’s what they see. The financial model mistake that kills climate pitches before the meeting starts. And the four structural differences between a real climate model and an adapted SaaS template.

They are buying everything. Are you selling? Four companies. 27 gigawatts contracted in 18 months. How the hyperscaler energy procurement wave is reshaping climate fundraising and which founders are positioned for it.

The term sheet is where the deal gets made or unmade. Most founders only find out which one after the exit. Use this before you sign.

-Yoann

Understand your term sheet

Below is the resource I still look over:

Keep reading with a 7-day free trial

Subscribe to Climate Insiders to keep reading this post and get 7 days of free access to the full post archives.