Read time: 4 min

The mega-exits are back. And they look nothing like 2021.

This week, newcleo announced it is going public on Nasdaq.

A $2.4 billion pre-money valuation. Up to $429 million in gross proceeds. PIPE oversubscribed at $10 per share.

If you read the climate trade press, this should not be happening.

We have spent 18 months being told climate is dead. ESG is over. The capital has rotated to AI. Founders should pivot.

Then this week, this happened.

What nobody is connecting

Two weeks ago, Fervo Energy IPO’d on Nasdaq.

Priced at $27. Raised $1.89 billion. Opened up 30%. Currently valued at around $10 billion.

The largest climate tech IPO of 2026. The largest energy IPO since 2013.

The killer detail buried in the S-1: Fervo has a 3 GW framework agreement with Google. Right of first refusal on new capacity through 2028. That single line is what made the IPO viable.

Now newcleo follows.

A lead-cooled fast modular reactor builder running on recycled nuclear waste. $755M already raised privately. SPAC-ing to public markets with strategic deployment money for Europe and the US.

And remember the pattern: NuScale via SPAC in 2022. Oklo via SPAC in 2024, now NYSE-listed. Fervo IPO May 2026. newcleo Nasdaq SPAC May 2026.

Rings The Opening Bell®")

Four exits. All in nuclear, geothermal, or advanced firm power.

This is not noise.

Why these specifically

Climate is not the same asset class it was three years ago.

Carbon credit startups raised $9 billion at peak in 2021 and most of those companies do not exist anymore.

What’s working in 2026 is different.

It is companies that sell firm, dispatchable, clean electrons to customers with infinite demand and limitless balance sheets.

Hyperscalers built the $725 billion AI capex wave. That wave needs power. Specifically: nuclear baseload, geothermal baseload, advanced firm capacity. 24/7. At scale.

I wrote about this last week in They are buying everything. Are you selling?

Four hyperscalers. 27 gigawatts contracted in 18 months.

That is the demand curve. Fervo and newcleo are what it looks like to be on the right side of it.

The new climate playbook

The exits coming this decade will not look like 2021.

No carbon SaaS. No accounting tools. No marketplaces.

The companies that exit are the ones that:

Sell electrons or molecules, not software

Have hyperscaler offtake agreements signed

Operate at gigawatt scale

Build real assets that throw off real cash

That is a very specific founder profile. And it is who public markets are now rewarding.

If you build clean firm power, advanced nuclear, geothermal, grid hardware, or any of the picks-and-shovels of the electron economy, this is your decade.

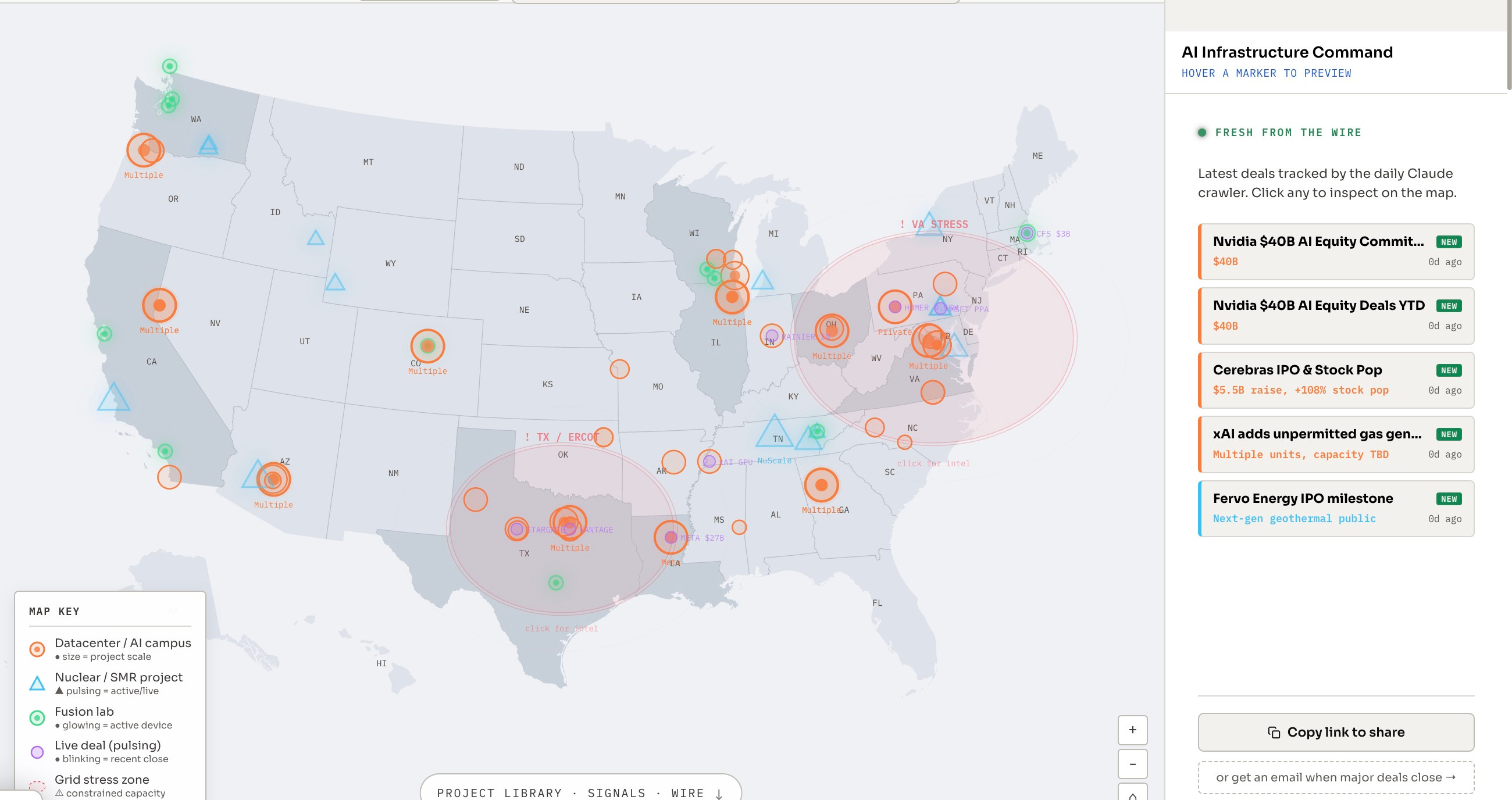

Track every deal as it happens on my AI Infrastructure Map. Top VC and PE analysts are using it daily. Activity has picked up like crazy in recent weeks.

Final thought

Climate is not dead.

Climate has been quietly reorganized around the only customer that matters right now: hyperscalers buying electrons faster than the grid can produce them.

The companies that read this signal in 2023 are listing in 2026.

The ones that read it in 2026 will list in 2029.

If you are raising right now and your story sits at the intersection of energy, AI, and firm power, this is the moment.

See you Tuesday for another unique resource.

—Yoann

🚨 Half my portfolio is now using VCboom (previously called Claude Fundraiser) to prep for the June raise window. The deck score alone is worth the seat. And it matches you automatically with the best investors across 47,000 angels, FOs and VCs. Promo code CODE20 for readers here.